Rules of Allocation

A careful and well-placed analysis of all expenditure and receipt is most necessary to effective financial control. It is the primary object of any accounting classification. It is necessary to secure uniformity of accounting to render suitable comparison between the accounts of different railways. It also helps in preparation of budget and estimates. The labor spent in the classification will be of no use if accounts office fails to maintain proper record as per prescribed classification or if the executive omits to review periodically with the assistance of such record of earning and expenditure for which they are responsible.

The primary responsibility for correct allocation of the initial record in support of receipts and payments rests with the executive offices. The account office is responsible for ensurance of correct allocation. Allocation is the process of indicating nature of expenditure (Head of accounts) under which expenditure is to be finally recorded.

CLASSIFICATION OF EXPENDITURE

The railway expenditure has been classified in to two groups namely: -

1) Capital Expenditure: Under this category such items of expenditure are included which pertain to acquisition of concrete assets, constructions, replacement and renewals of assets such as cost of land, Construction of staff quarters, Construction of Bridges etc.

Expenditure incurred on amenities to passengers and other railway users, amenities to staff, unremunerative operating improvement works when incurred on acquiring concrete assets is not treated as capital expenditure but is accounted for separately under “Development Fund” and “Open Line Works Revenue”.

The Expenditure on renewals and replacements of railway assets is made out from a separate fund commonly known as “Depreciation Reserve Fund”. For the purpose of revenue allocation the revenue

working expenses for the railways are classified under thirteen major heads with a separate abstract for each sub major head.

2) REVENUE EXPENDITURE: - These items of expenditure relate to the

working of railway, repairs and maintenance and operation of rolling stock, Plant and Machinery and equipment’s.

The items of expenditure which are incurred on repairs and maintenance of various assets such as railway track, bridges, service and residential buildings etc. are in the nature of day to day expenses. To keep the

organization running and also to enable the existing assets to give the same services and to keep them in good service condition for achieving the above purpose the revenue working expenses of the railways has

been classified in to thirteen abstracts and each abstract being given a different alphabet to identity the expenditure.

From first April of 1979 the entire structure of railways Demands for Grants and the classification of earning and expenditure has undergone complete revision and accordingly Revenue abstracts have been utilized for recording the revenue working expenses. The Demands have been further classified in to main heads, sub heads and detailed heads to form the allocation for any expenditure. The allocation will be in eight digits, which will in three parts.

From first April of 1979 the entire structure of railways Demands for Grants and the classification of earning and expenditure has undergone complete revision and accordingly Revenue abstracts have been utilized for recording the revenue working expenses. The Demands have been further classified in to main heads, sub heads and detailed heads to form the allocation for any expenditure. The allocation will be in eight digits, which will in three parts.

Part I: - This part gives the demand applicable as per the nature of expenditure and consists of First 3 digits. The same can also be denoted by corresponding abstract applicable to the demand.

Part II: - Second group of three numerical digits indicate the main head of account which individually indicate the minor head, sub head and detailed head respectively.

Part III: - This part consist of two numerical digits which represents the primary unit i.e. object of expenditure.

Capital nature of expenditure is mainly divided in to five heads of allocation i.e. Capital, DRF, DF, OLWR and Capital Fund.

Capital nature of expenditure is mainly divided in to five heads of allocation i.e. Capital, DRF, DF, OLWR and Capital Fund.

The introduction, abolition and change of nomenclature of any main/sub head or transfer of detailed head from one main head of one group to any other group or re-arrangement of the abstract is not within the power of Railway Administration. FA&CAO with the approval of GM may open a new detail head or sub head in extreme emergency.

PRIMARY UNITS

01 Salaries and Wages

02 Dearness allowance

03 Productivity linked bonus

04 House rent allowance

05 City compensatory allowance

09 Wages of casual labors

10 Mileage or K.M. allowance

11 Over Time allowance

12 Night Duty allowance

13 Other allowances

14 Fees and Honorarium

15 Transfer allowance

16 Travelling allowance including air travel

17 Air travel expenses sanctioned in lieu of privilege passes

18 Office expenses

19 Rent for P & T, Telephone charges including trunk calls.

21 Advertisement expenses.

22 Utilities water, electricity etc.

23 Rental for office equipment other than data processing.

24 Printing and stationary including publications.

27 Cost of material from stock.

28 Cost of material direct purchases.

31 Fuel for other than traction.

32 Contractual payments.

33 Transfer of debits and credits from one unit to another.

34 Adjustment of wages on POH and other repairs from WMS account to revenue heads.

36 Excise duty for purchases of material.

37 Customs duty

38 Sales tax.

39 Other expenses.

The following primary units are used for expenditure for works: -

1 Pay and allowance

2 Payments to casual labor.

3 Payments to contractors.

4 Direct supply of material.

5 Stores supplied from stock.

6 Freight on stores.

7 Credit for released material.

8 Others.

9 Transfer of debits/credits effecting Capital Works Expenditure.

10 P.L.B.

11 Excise duty for purchases of material.

12 Custom duty.

13 Sales Tax.

The revised classification of expenditure on works irrespective of whether they are charged to capital, DRF, DF, OLWR will come under single demand no 16 namely Assets acquisition, construction and replacement.

The accounting classification for works expenditure is in the form of 7 digits 4-module alphabetical code.

The first module which is an alpha indicates the source of fund namely capital, DRF, DF, OLWR as the case may be.

The second module of 2-digits is numerical this will represent the standard plan head.

The third module, which is also numerical, will represent the two digits corresponding to the sub-detailed head of classification giving the details of the asset acquired, constructed or replaced.

The last module, which is also numerical 2-digit module, will indicate the primary unit or object of expenditure.

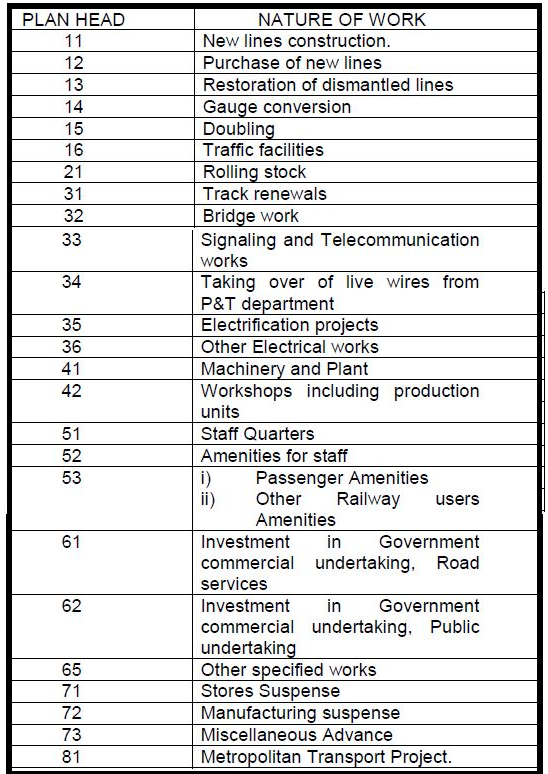

The following plan heads are often used under demand no 16. These are also known as minor heads or plan heads.

The heads of accounts are financed from

CAPITAL: Loan from General Revenues.

DRF, DF, and CAPITAL FUND: Internal Resources.

OLWR, REVENUE: Current Revenue.

Expenditure incurred for creation/acquisition of assets for the purpose of earnings or possession is termed as capital expenditure

CAPITAL.

Capital bears/is debited with: -

1) The costs of land other than for quarrying and mining purpose.

2) The first cost of construction and equipment of a line under construction whether commercial or strategic whether remunerative or unremunerative and New production unit.

3) The cost of maintenance of a section of a line under construction not opened for traffic.

4) The cost of any additions to the line or equipment estimated to cost more than Rs1/- lakh (New Minor Works Limit) when not chargeable to DF or OLWR.

5) The full cost of replacement of an asset where the original cost was charged to revenue, being within New Minor Works Limit but is now more than Rs1/- lakh provided it is not chargeable to DF or OLWR.

6) The cost of any additional plant and machinery not connected with any specific work where it exceeds the New Minor Works Limit.

7) The cost of any tools and plant specially purchased and any post specially created for the supervision or construction of a work chargeable purely to capital.

8) The cost of construction and equipment of unremunerative new lines (Other than Rolling stock and Land) and the cost of Maintenance of a section of new line not opened for traffic though remunerative.

9) The cost of Quarters w.e.f. 1.4.1974 onwards including the cost of fans and other amenities in type I and II Railway quarters constructed prior to 1.4.1974

Capital is credited with : -

1) The cost at the debit of capital of any Asset (other than land) which is abandoned or disposed off without being replaced.

2) The sale proceeds of any land acquired at the cost of capital when it is sold or surrendered.

3) The difference between the cost at the debit of capital of a replaced asset and the cost of its replacement, when the cost of replacement is chargeable to DRF and is less than the cost at the debit of capital.

4) The cost of labour originally incurred in laying the assets or part thereof, when such items are subsequently transferred for the use on a new work.

5) The original cost at the debit of capital of an asset replaced at the cost of OLWR / DRF.

Capital fund.

The existing Revenue Reserve Fund has been abolished, with effect from 1992-93. In order to reduce over capitalization and to enable Railways to raise internal resources for meeting their increasing requirements for

capital expenditure a new fund “CAPITAL FUND” has been created. This fund will bear the expenditure hither to chargeable to capital subject to availability of funds and provision in the sanctioned budget.

The expenditure on plan head 12 to 16, 21, 31, 32, 34 to 36, 41, 42,52,53, 61, 62, 64 will be financed from the capital fund where as expenditure on plan head 11 (New lines) 51(Staff quarters) 81 (MTP) will

continue to be financed from the loan capital i.e. General Revenue.

Depreciation Reserve Fund.

In order to meet the cost of replacement of an asset, the normal life of which is over, due to wear and tear and requires replacement, DRF has been created.

Depreciation Reserve Fund bears / is debited with

1) The cost of Replacement and Renewals of works whether originally provided from Capital, Development Fund, Capital Fund.

2) The costs of replacement of ballast involving improved type of ballast.

3) The original cost of an asset at the debit of capital (other than land) replaced at the cost of OLWR.

4) The cost at the debit of capital or DF of an asset (other than land) which is abandoned or disposed off without being replaced.

5) All expenditure incurred on replacement of Rolling Stock.

6) The cost of tools and plant specially purchased and of any post specially created for the supervision of a work purely chargeable to DRF.

NOTE. Replacement of assets created out of OLWR is chargeable to OLWR if the cost of replacement is not more than Rs1/- lakh.

Depreciation Reserve Fund is Credited with : -

1) The amount of annual contribution from the Railway Revenue.

2) The amount realized from the disposal of an asset ( at the debit of capital or DF ) the original cost of which is more than RS 5000 and the amount realized from the disposal of the materials, released from a

work, replaced at the cost of DRF, after deducting the incidental charges.

3) The amount of interest earned on the balance of the fund.

Development Fund

In order to arrest over capitalization of Railway undertaking the government have decided that all un-remunerative new lines, works for passengers amenities, staff welfare and amenities works, operational

improvement works should be charged to this fund. This fund was instituted with effect from 1/4/1950.

Development Fund is Debited with

DF I The cost of all passenger and other user's amenity works including additions and replacement of the existing and new works.

DF II Cost of Labour Welfare Works including additions to existing and new works when cost is exceeding Rs1,00,000/-

The cost of construction of staff quarters including additions to existing quarters will be charged to capital with effect from 1/4/1974.

DF III The entire cost of works when exceeding RS 10/- lakhs which are un-remunerative but are required for improvement of operational efficiency including additions and alterations, replacement of existing and new

works.

DF IV Safety works.

Development fund is credited with

1) Amount transferred from Revenue Reserve Fund.

2) The amount appropriated to it each year from surplus.

3) The cost at the debit of DF of an asset which is abandoned or disposed off without being replaced.

4) The difference between the cost at the debit of DF of replaced asset and the cost of its replacement when the cost of replacement is chargeable to DRF and is less than the cost at the debit of DF.

5) The amount of interest earned on the balance of the fund.

Open Line Works Revenue

This head is financed from Revenue and bears / debited with

1) Cost of all works other than those related with passenger and other users amenity works chargeable to DF whether new, additional improvements, replacement and renewal works when the cost is less than RS 1,00,000/- i.e. within the limit of new minor works.

2) Cost of such replacement and renewals costing less than RS 1,00,000/- when not chargeable to capital, capital fund, DRF, DF, and Revenue.

3) The cost of all un-remunerative works for improving the operational efficiency when the cost is less than RS 10/- Lakhs.

4) The cost of dismantling handling and shifting including freight to stores depot in respect of replacement works.

5) The expenditure on investment in share capital of Railwaymen’s consumer Co-operative societies up to RS 2,500/- per society.

OLWR is credited with the amount realized from disposal of an asset without being replaced, the original cost of which was charged to OLWR and amount realized from disposal of the asset replaced at the cost of

OLWR.

List of passenger amenities.

1) Provision of overhead and ground level arrangement at stations for filling water in carriages, water supply at stations including purification plants water coolers, or water trolleys provided at stations.

2) Provision of waiting accommodation including provision of benches and improvement to the existing arrangements.

3) Provision of refreshment rooms, retiring rooms, vendor stalls of all description except those which are required to be provided by the contractors themselves.

4) Provision for improvements to latrines provided at stations for the use of bonafide Railway passengers.

5) Provision of bathing facility at station for use of passengers.

6) Improvement to existing carriages such as provision of fans improved lighting, bigger water tanks etc intended to provide improved facilities to passengers.

7) Improved lighting and provision of fans on platforms or in waiting hall and sheds etc. to cater to the requirements of Railway passengers.

8) Exhibition of sheet time table in glass frame or on black board to cater to the requirements of the passenger.

9) Works under all the above heads meant to cater the Railway passengers during religious fare (mela) required for a period exceeding six months.

Other Railway users amenities.

The persons availing the facility of parcels or goods services are termed as other Railway users. The facilities provided at parcel office or goods sheds can be termed as other Railway users amenities.

1) Arrangement for drinking water including water coolers, water trolley etc.

2) Waiting accommodation including provision of various types of premises.

3) Refreshment rooms including vendor stalls except those which are required to be provided by the contractors themselves.

4) Provision of latrines or urinals.

5) Lighting arrangement and provision of fans.

6) Any other work considered essential i.e. inquiry office, information Centre etc.

Labour Welfare Works.

The works which are carried out as a welfare measure for the work force in general are called as Labour welfare works. The list of labour welfare works is as under.

1) Provision of new hospitals, dispensaries, school etc. Additions, Alterations and improvements to the existing work.

2) Provision of new institutes, recreation rooms, swimming pools, sports ground, reading rooms including improvements to the existing ones.

3) Provision ad improvements to health and welfare services, child welfare and maternity centers, cooling arrangements for workshops and rest rooms for workmen.

4) Provision and improvements of sanitation water supply, road lighting and marketing facilities in Railway colonies.

Un-remunerative works but essential for increasing operational efficiency.

Works arising out of the need for keeping operational methods upto the latest requirements and standards are as under.

1) Removal of infringement at stations.

2) Re grading of permanent way and improvements to curves.

3) Converting dead end sidings into through routes and provision of through loops at station.

4) Provision, extension and modernization of catch sidings.

5) Lighting of sheds and stations whether new works or improvement to existing works.

6) Duplicating or strengthening girders by adding material.

7) Provision and improvements and additions to drivers and guards running rooms.

8) Provision of fire fighting equipments at stations.